Why This Confusion Costs Seniors Thousands of Dollars

Medicare and Medicaid are two of the most important programs in any American senior’s financial plan. They are also two of the most widely confused. Many families do not discover that Medicaid covers nursing home care until they are already in a crisis situation, long past the point at which Medicaid planning could have protected family assets.

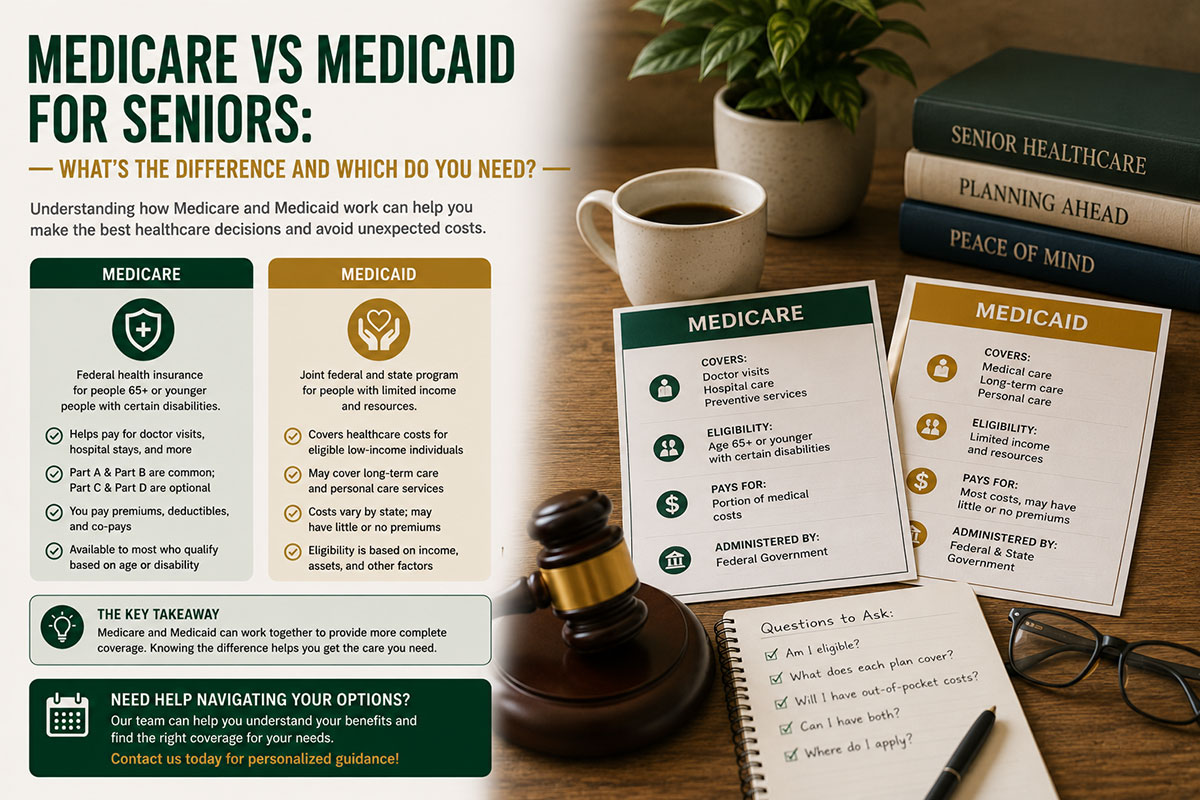

Medicare: What It Is, Who Qualifies, and What It Covers

Medicare is a federal health insurance program primarily for Americans 65 and older. Medicare is not means-tested — eligibility is based on age and work history, not income or assets. If you (or your spouse) have paid Medicare taxes for at least 10 years (40 quarters) of work, you are entitled to Medicare at 65.

Medicare Part A: Hospital Insurance

Medicare Part A covers inpatient hospitalisation, skilled nursing facility care (under specific qualifying conditions and time limits), some home health care, and hospice care. Most people pay no premium for Part A if they have the required work history. The 2026 inpatient deductible is $1,676 per benefit period.

Medicare Part B: Medical Insurance

Medicare Part B covers outpatient medical care — doctor visits, outpatient procedures, preventive services, and some home health services. Part B requires a monthly premium ($185.00 in 2026 for most enrollees) and has an annual deductible ($257 in 2026). After meeting the deductible, Part B typically covers 80% of approved costs.

Medicare Part C: Medicare Advantage

Medicare Advantage is an alternative to traditional Medicare provided by private insurance companies. Advantage plans bundle Part A and Part B coverage (and usually Part D) into a single plan, often with additional benefits (dental, vision, hearing) but with more network restrictions.

Medicare Part D: Prescription Drug Coverage

Medicare Part D covers prescription drugs through private insurance plans. The 2026 out-of-pocket cap for prescription drugs under Part D is $2,000, a significant improvement for high-cost drug users under the Inflation Reduction Act changes.

Medicaid: What It Is, Who Qualifies, and What It Covers

Medicaid is a joint federal-state program that provides health coverage to low-income individuals of all ages. For seniors specifically, Medicaid’s most significant role is as the primary payer for long-term custodial care — the nursing home and assisted living care that Medicare does not cover.

Unlike Medicare, Medicaid is means-tested. In most states, an individual must have very limited assets — typically $2,000 or less in countable assets — to qualify for Medicaid long-term care benefits.

Key Differences: Medicare vs Medicaid Side by Side

| Feature | Medicare | Medicaid |

| Eligibility | Age 65+ based on work history | Low-income individuals of any age |

| Funding | Primarily federal | Federal + state governments |

| Senior Coverage | Acute medical care & short-term rehab | Long-term custodial care |

| Means Tested? | No | Yes |

| Long-Term Care | Does NOT cover custodial care | Primary public payer for LTC |

Can You Have Both? Dual Eligibility Explained

Yes. Individuals who qualify for both Medicare and Medicaid are called ‘dual eligibles.’ For dual-eligible individuals, Medicare pays first for covered services, and Medicaid covers costs that Medicare does not — including premiums, co-payments, and the long-term care services that Medicare excludes.

Enrollment Periods: When to Sign Up and Why Timing Matters

The Initial Enrollment Period for Medicare is the seven-month window surrounding your 65th birthday. Missing Part B enrollment during this window results in a permanent 10% premium increase for each 12-month period you were eligible but not enrolled — and this penalty lasts for the rest of your life.